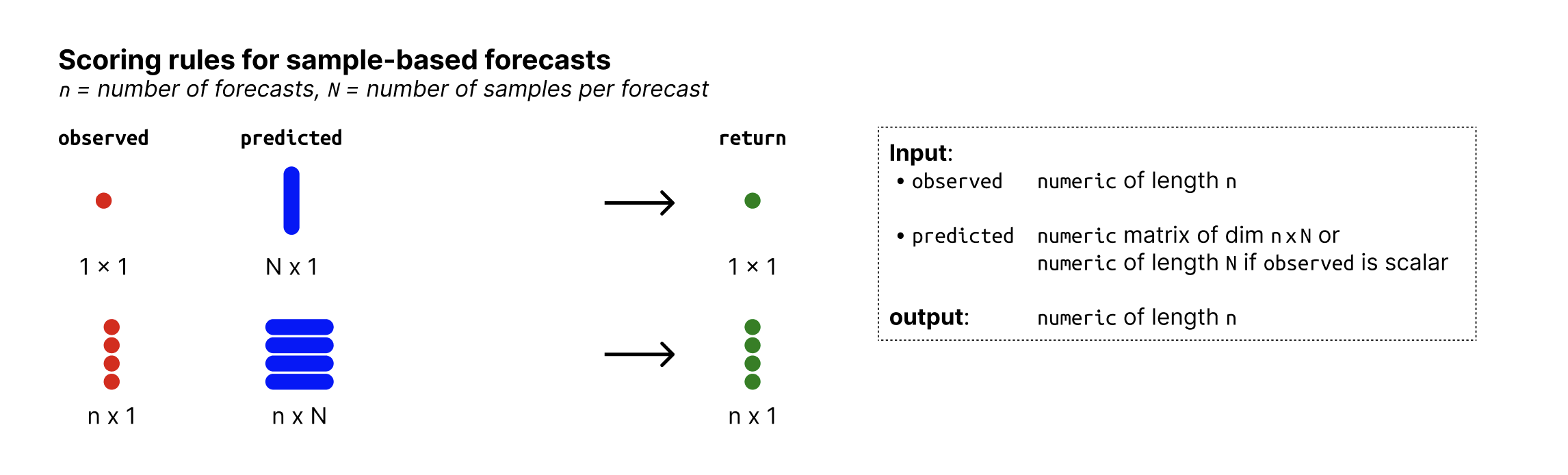

Determines bias from predictive Monte-Carlo samples. The function automatically recognises whether forecasts are continuous or integer valued and adapts the Bias function accordingly.

Value

Numeric vector of length n with the biases of the predictive samples with respect to the observed values.

Details

For continuous forecasts, Bias is measured as

$$ B_t (P_t, x_t) = 1 - 2 * (P_t (x_t)) $$

where \(P_t\) is the empirical cumulative distribution function of the prediction for the observed value \(x_t\). To handle ties appropriately (which can occur when predictions equal observations for exampele due to rounding), \(P_t(x_t)\) is computed using mid-ranks: the fraction of predictive samples strictly smaller than \(x_t\) plus half the fraction equal to \(x_t\).

For integer valued forecasts, Bias is measured as

$$ B_t (P_t, x_t) = 1 - (P_t (x_t) + P_t (x_t + 1)) $$

to adjust for the integer nature of the forecasts.

In both cases, Bias can assume values between -1 and 1 and is 0 ideally.

References

The integer valued Bias function is discussed in Assessing the performance of real-time epidemic forecasts: A case study of Ebola in the Western Area region of Sierra Leone, 2014-15 Funk S, Camacho A, Kucharski AJ, Lowe R, Eggo RM, et al. (2019) Assessing the performance of real-time epidemic forecasts: A case study of Ebola in the Western Area region of Sierra Leone, 2014-15. PLOS Computational Biology 15(2): e1006785. doi:10.1371/journal.pcbi.1006785

Examples

## integer valued forecasts

observed <- rpois(30, lambda = 1:30)

predicted <- replicate(200, rpois(n = 30, lambda = 1:30))

bias_sample(observed, predicted)

#> [1] 0.660 -0.025 0.710 -0.930 0.870 0.435 -0.885 -0.940 -0.515 -0.790

#> [11] 0.975 -0.975 -0.620 -0.740 -0.640 0.395 0.695 -0.765 -0.935 -0.680

#> [21] -0.725 -0.320 0.355 0.730 0.250 0.995 -0.650 0.235 0.250 0.850

## continuous forecasts

observed <- rnorm(30, mean = 1:30)

predicted <- replicate(200, rnorm(30, mean = 1:30))

bias_sample(observed, predicted)

#> [1] -0.46 0.02 0.02 0.12 -0.18 -0.07 0.96 -0.60 0.16 -0.31 0.79 0.49

#> [13] -0.74 -0.48 0.26 -0.56 0.82 0.89 0.41 -0.31 0.19 0.47 -0.85 0.32

#> [25] 0.15 -0.16 0.34 -0.30 0.80 0.27