library(forecastbaselines)

library(scoringutils)

library(ggplot2)

setup_ForecastBaselines()

#> Instantiating Julia project: /home/runner/work/_temp/Library/forecastbaselines/julia

#> Starting Julia ...

#> Loading Julia bridge: forecast_helpers.jl

#> forecastbaselines setup complete!Overview

forecastbaselines provides 10 baseline forecasting models across three categories:

- Simple Baselines - Naive methods for benchmarking

- Seasonal/Trend Models - For patterned data

- Advanced Time Series Models - Statistical models

This vignette provides:

- Detailed description of each model

- When to use each model

- Parameter guidance

- Practical examples

- Performance characteristics

Model Selection Guide

Quick Decision Tree

Do you have seasonal patterns?

├─ Yes, strong seasonality

│ ├─ Regular pattern → STLModel(s = period)

│ ├─ Irregular pattern → LSDModel(window_width, s = period)

│ └─ Need decomposition → STLModel(s = period)

├─ No, mostly trend

│ ├─ Polynomial trend → OLSModel(degree)

│ ├─ Step changes → IDSModel(window_size)

│ └─ Complex trend → ARMAModel(p, q)

└─ No clear pattern

├─ Need simple baseline → ConstantModel()

├─ Sample from history → MarginalModel()

└─ Smooth estimates → KDEModel()

Special cases:

- Count data (integers) → INARCHModel(p)

- Multiple components → ETSModel(error_type, trend_type, season_type)

- Quick benchmark → ConstantModel()Model Comparison Table

| Model | Complexity | Data Needs | Seasonality | Trend | Prob. Forecasts |

|---|---|---|---|---|---|

| Constant | Very Low | Minimal (1+) | No | No | Via residuals |

| Marginal | Very Low | 30+ | No | No | Direct |

| KDE | Low | 50+ | No | No | Direct |

| LSD | Low | 2+ cycles | Yes | No | Via residuals |

| OLS | Low | 20+ | No | Yes | Via residuals |

| IDS | Low | 20+ | No | Yes | Via residuals |

| STL | Medium | 2+ cycles | Yes | Yes | Via residuals |

| ARMA | Medium | 50+ | No | No | Parametric |

| INARCH | Medium | 50+ | Yes | No | Parametric |

| ETS | High | 50+ | Yes | Yes | Parametric |

1. Simple Baseline Models

These models provide quick, interpretable forecasts and serve as benchmarks for more complex methods.

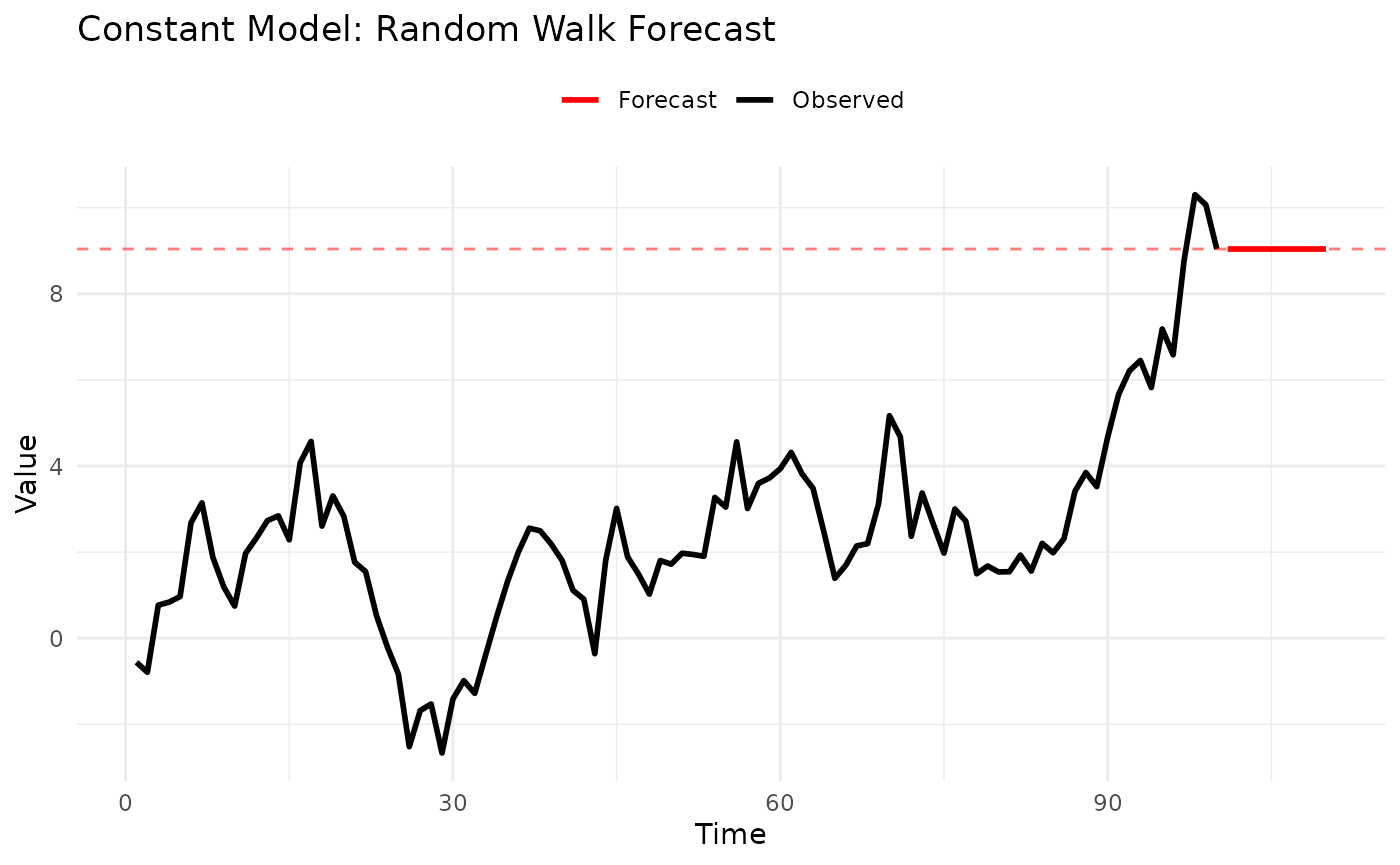

1.1 Constant Model (Naive Forecast)

Description: The simplest possible forecast - uses the last observed value for all future predictions.

Mathematical Form:

When to Use:

- ✅ Quick baseline for model comparison

- ✅ Random walk data (financial prices, etc.)

- ✅ When you need fast, simple forecasts

- ❌ Data with trends or seasonality

Parameters: None - completely parameter-free.

Example:

# Generate random walk data

set.seed(123)

data <- cumsum(rnorm(100))

# Fit constant model

model <- ConstantModel()

fitted <- fit_baseline(data, model)

# Forecast

fc <- forecast(fitted, interval_method = NoInterval(), horizon = 1:10)

# Visualize

n_data <- length(data)

plot_df <- rbind(

data.frame(time = 1:n_data, value = data, type = "Observed"),

data.frame(time = 101:110, value = fc$mean, type = "Forecast")

)

ggplot(plot_df, aes(x = time, y = value)) +

geom_line(aes(color = type), linewidth = 1) +

geom_hline(yintercept = data[100], linetype = "dashed", color = "red", alpha = 0.5) +

scale_color_manual(values = c("Observed" = "black", "Forecast" = "red")) +

labs(title = "Constant Model: Random Walk Forecast", x = "Time", y = "Value", color = NULL) +

theme_minimal() +

theme(legend.position = "top")

Strengths:

- Extremely fast

- No parameters to tune

- Optimal for random walks

- Easy to explain

Limitations:

- Ignores all patterns

- Flat forecast function

- Poor for trending/seasonal data

1.2 Marginal Model

Description: Forecasts by randomly sampling from the empirical distribution of the observed data.

Mathematical Form:

When to Use:

- ✅ Stationary data without autocorrelation

- ✅ Need probabilistic forecasts

- ✅ Distribution shape matters more than sequence

- ❌ Trending or seasonal patterns

- ❌ Strong autocorrelation

Parameters: None

Example:

# Generate stationary data

set.seed(123)

data <- rnorm(100, mean = 50, sd = 10)

# Fit marginal model

model <- MarginalModel()

fitted <- fit_baseline(data, model)

# Forecast with prediction intervals

fc <- forecast(

fitted,

interval_method = EmpiricalInterval(n_trajectories = 1000),

horizon = 1:10,

levels = c(0.5, 0.95),

model_name = "Marginal"

)

# The forecast mean approximates the historical mean

cat("Historical mean:", mean(data), "\n")

#> Historical mean: 50.90406

cat("Forecast mean:", mean(fc$mean), "\n")

#> Forecast mean: 50.90406

# Quantile forecasts are now available for scoring

set.seed(124)

truth <- 50 + rnorm(10, 0, 10) # Simulated future values

fc_truth <- add_truth(fc, truth)

# Convert to quantile format and show structure

fc_quantile <- scoringutils::as_forecast_quantile(fc_truth)

print(head(fc_quantile, 15)) # Show first few quantiles

#> observed predicted quantile_level horizon model

#> <num> <num> <num> <int> <char>

#> 1: 36.14929 33.76226 0.025 1 Marginal

#> 2: 36.14929 45.25548 0.250 1 Marginal

#> 3: 36.14929 51.31836 0.500 1 Marginal

#> 4: 36.14929 58.49046 0.750 1 Marginal

#> 5: 36.14929 72.09168 0.975 1 Marginal

#> 6: 50.38323 33.63193 0.025 2 Marginal

#> 7: 50.38323 45.92043 0.250 2 Marginal

#> 8: 50.38323 52.43278 0.500 2 Marginal

#> 9: 50.38323 58.97530 0.750 2 Marginal

#> 10: 50.38323 72.09168 0.975 2 Marginal

#> 11: 42.36970 33.63193 0.025 3 Marginal

#> 12: 42.36970 45.12309 0.250 3 Marginal

#> 13: 42.36970 50.76936 0.500 3 Marginal

#> 14: 42.36970 57.41528 0.750 3 Marginal

#> 15: 42.36970 70.98152 0.975 3 MarginalStrengths:

- Captures full distribution

- Natural uncertainty quantification

- No distributional assumptions

Limitations:

- Ignores temporal dependence

- Requires sufficient data (30+)

- Constant forecast on average

Use Case: Benchmark for comparing autocorrelation benefits. If ARMA doesn’t beat Marginal, your data may not have useful autocorrelation.

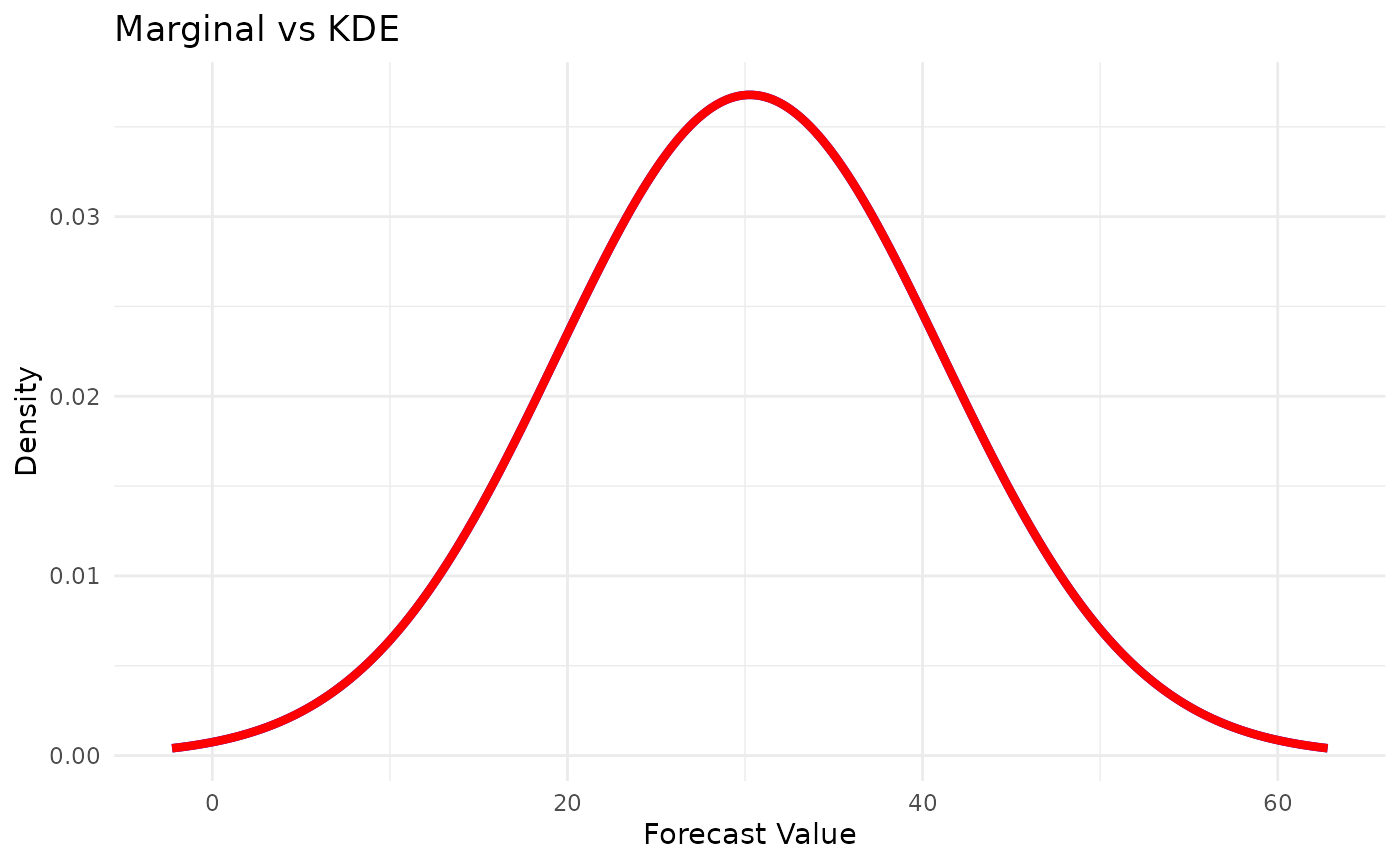

1.3 KDE Model (Kernel Density Estimation)

Description: Similar to Marginal but uses kernel density estimation for smoother probability distributions.

Mathematical Form:

where is a kernel function and is bandwidth.

When to Use:

- ✅ Need smooth probability estimates

- ✅ Continuous data

- ✅ Multi-modal distributions

- ❌ Small sample sizes (< 50)

- ❌ Discrete/count data

Parameters: None (bandwidth selected automatically)

Example:

# Generate bimodal data

set.seed(123)

data <- c(

rnorm(50, mean = 20, sd = 3),

rnorm(50, mean = 40, sd = 3)

)

# Compare Marginal vs KDE

marginal <- fit_baseline(data, MarginalModel())

kde <- fit_baseline(data, KDEModel())

fc_marginal <- forecast(marginal, interval_method = NoInterval(), horizon = 1:100)

fc_kde <- forecast(kde, interval_method = NoInterval(), horizon = 1:100)

# KDE produces smoother samples

# Prepare data for ggplot

marginal_density <- density(fc_marginal$mean)

kde_density <- density(fc_kde$mean)

density_df <- rbind(

data.frame(x = marginal_density$x, y = marginal_density$y, type = "Marginal"),

data.frame(x = kde_density$x, y = kde_density$y, type = "KDE")

)

ggplot(density_df, aes(x = x, y = y, color = type)) +

geom_line(linewidth = 1.5) +

scale_color_manual(values = c("Marginal" = "red", "KDE" = "blue")) +

labs(title = "Marginal vs KDE", x = "Forecast Value", y = "Density", color = NULL) +

theme_minimal() +

theme(legend.position = "topright")

Strengths:

- Smooth probability estimates

- Handles multi-modal data

- Good for continuous distributions

Limitations:

- Needs more data than Marginal (50+)

- Computationally more expensive

- Still ignores autocorrelation

2. Seasonal and Trend Models

For data with identifiable patterns in time.

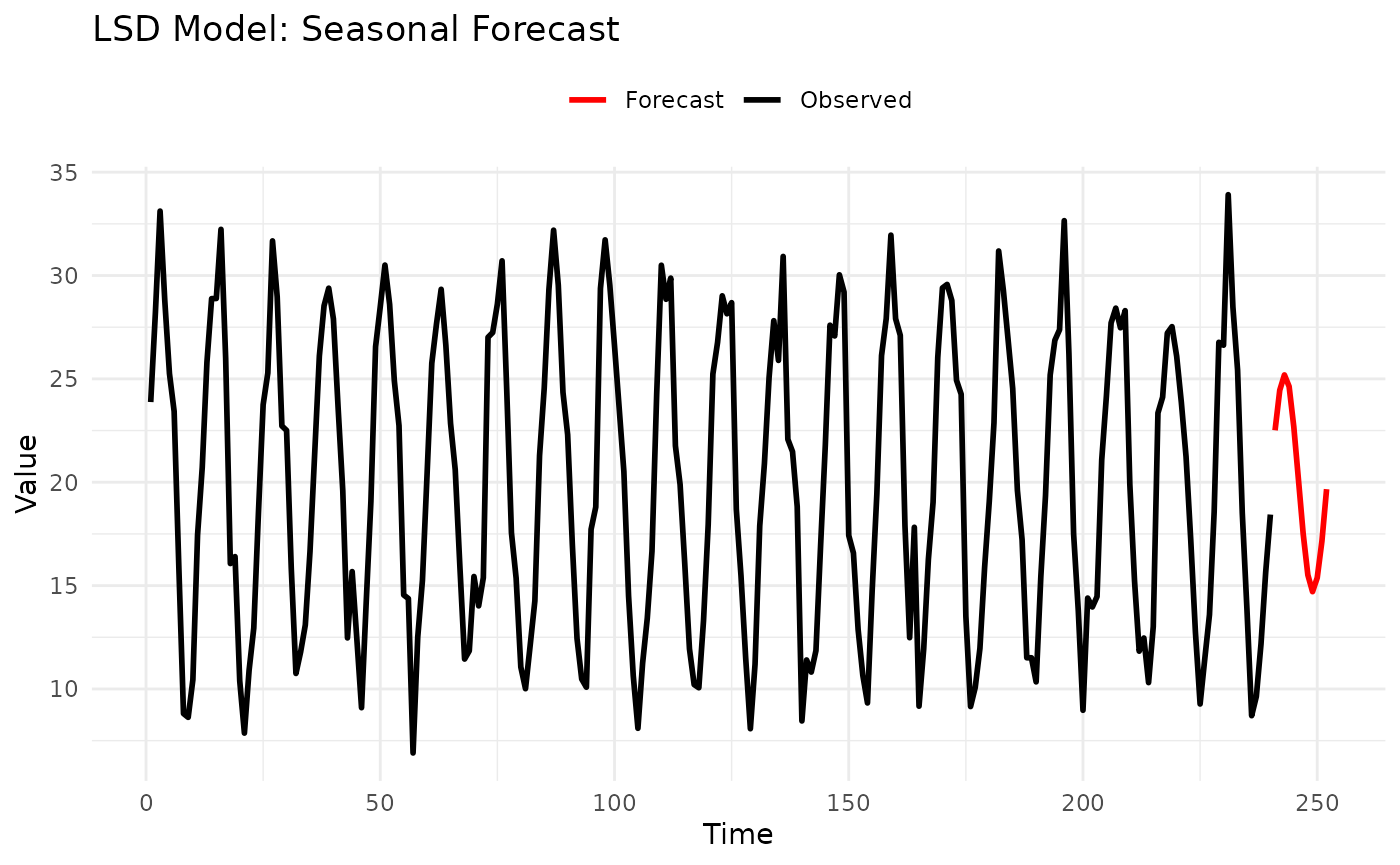

2.1 LSD Model (Last Similar Dates)

Description: Seasonal model that forecasts by averaging values from similar historical periods.

How It Works:

- For horizon , look back to periods , , etc.

- Average the

windowmost recent similar periods - Handles irregular seasonality well

When to Use:

- ✅ Strong seasonal patterns

- ✅ Seasonality more important than trend

- ✅ Irregular seasonal effects

- ❌ Purely trending data

- ❌ Less than 2 full seasonal cycles

Parameters:

-

window: Number of similar periods to average (default: 1) -

s: Seasonal period (e.g., 12 for monthly, 7 for daily)

Example:

# Monthly data with seasonality

set.seed(123)

months <- 1:240

seasonal_pattern <- 20 + 10 * sin(2 * pi * months / 12)

data <- seasonal_pattern + rnorm(240, sd = 2)

# Fit LSD model

model <- LSDModel(window_width = 3, s = 12) # Average last 3 years

fitted <- fit_baseline(data, model)

# Forecast next year

fc <- forecast(fitted, interval_method = NoInterval(), horizon = 1:12)

# Plot

n_data <- length(data)

plot_df <- rbind(

data.frame(time = 1:n_data, value = data, type = "Observed"),

data.frame(time = 241:252, value = fc$mean, type = "Forecast")

)

ggplot(plot_df, aes(x = time, y = value, color = type)) +

geom_line(linewidth = 1) +

scale_color_manual(values = c("Observed" = "black", "Forecast" = "red")) +

labs(title = "LSD Model: Seasonal Forecast", x = "Time", y = "Value", color = NULL) +

theme_minimal() +

theme(legend.position = "top")

Parameter Guidance:

-

s(seasonal period):- 7 for daily data with weekly patterns

- 12 for monthly data with yearly patterns

- 24 for hourly data with daily patterns

- 52 for weekly data with yearly patterns

-

window(averaging window):- 1: Use only last similar period (more responsive)

- 3-5: Smooth average (more stable)

- Large: Very smooth but less adaptive

Strengths:

- Simple and interpretable

- Handles irregular seasonality

- Fast computation

- Works with little data

Limitations:

- No trend modeling

- Needs at least 2 seasonal cycles

- Fixed seasonal period

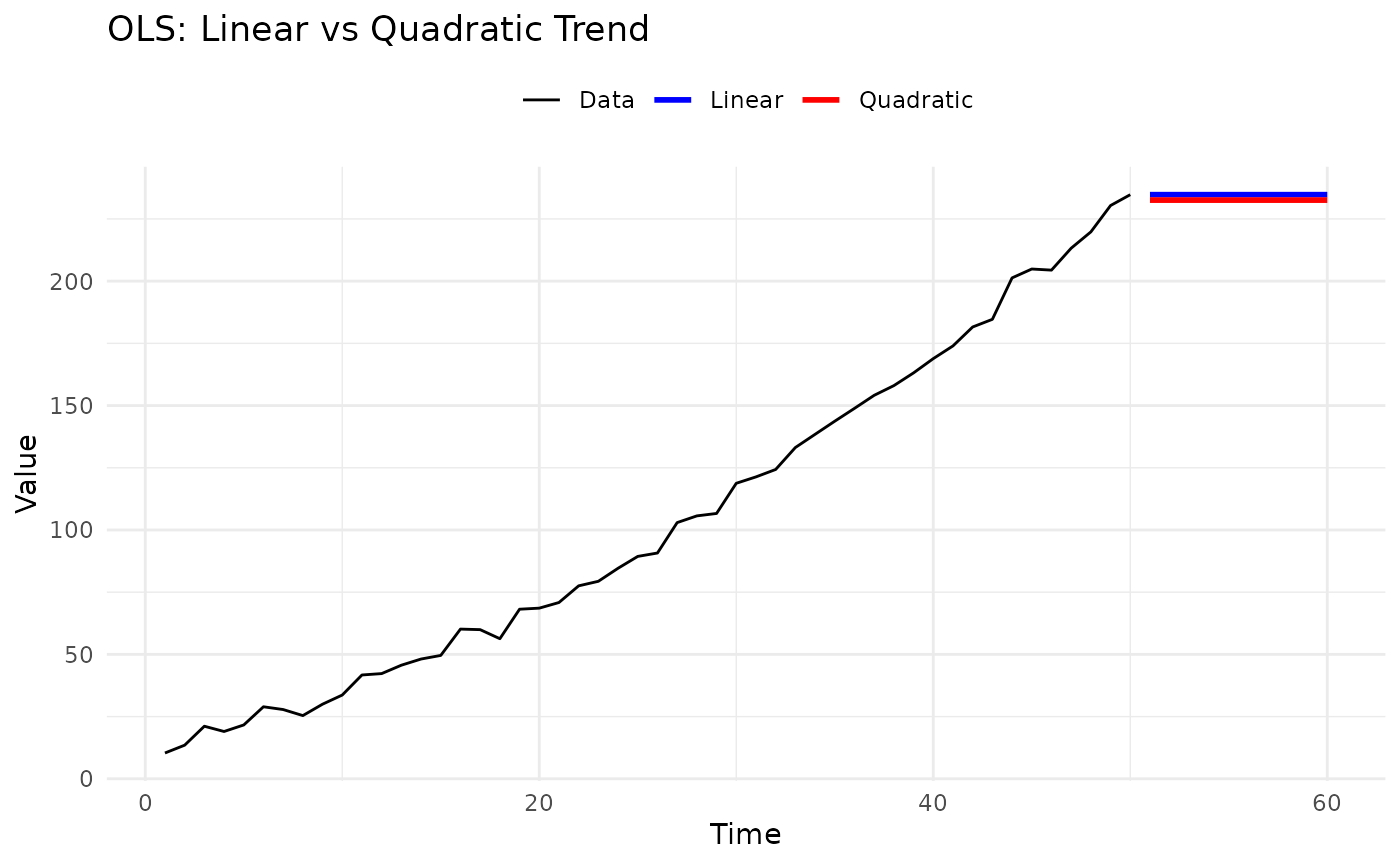

2.2 OLS Model (Polynomial Trend)

Description: Fits polynomial trends using ordinary least squares, then forecasts by extrapolating the trend.

Mathematical Form:

When to Use:

- ✅ Clear polynomial trends

- ✅ Smooth, continuous trends

- ✅ Short-term extrapolation

- ❌ Seasonal patterns

- ❌ Long-term forecasts (unstable extrapolation)

Parameters:

-

degree: Polynomial degree (1 = linear, 2 = quadratic, etc.) -

differencing: Order of differencing (default: 0)

Example:

# Generate quadratic trend

set.seed(123)

time <- 1:50

data <- 10 + 2 * time + 0.05 * time^2 + rnorm(50, sd = 3)

# Compare linear vs quadratic

linear <- fit_baseline(data, OLSModel(degree = 1))

quadratic <- fit_baseline(data, OLSModel(degree = 2))

fc_linear <- forecast(linear, interval_method = NoInterval(), horizon = 1:10)

fc_quadratic <- forecast(quadratic, interval_method = NoInterval(), horizon = 1:10)

# Plot

n_data <- length(data)

plot_df <- rbind(

data.frame(time = 1:n_data, value = data, type = "Data"),

data.frame(time = 51:60, value = fc_linear$mean, type = "Linear"),

data.frame(time = 51:60, value = fc_quadratic$mean, type = "Quadratic")

)

ggplot(plot_df, aes(x = time, y = value, color = type)) +

geom_line(aes(linewidth = type)) +

scale_linewidth_manual(values = c("Data" = 0.5, "Linear" = 1, "Quadratic" = 1)) +

scale_color_manual(values = c("Data" = "black", "Linear" = "blue", "Quadratic" = "red")) +

labs(title = "OLS: Linear vs Quadratic Trend", x = "Time", y = "Value", color = NULL, linewidth = NULL) +

theme_minimal() +

theme(legend.position = "top")

Parameter Guidance:

-

degree:- 1: Linear trend (most common)

- 2: Quadratic (turning point)

- 3: Cubic (S-shaped curves)

- 4+: Rarely recommended (overfitting risk)

-

differencing:- 0: Model in levels

- 1: Model in first differences

- Requires

degree >= differencing + 1

Strengths:

- Simple interpretation

- Fast computation

- Well-understood statistics

Limitations:

- Polynomial extrapolation can be unstable

- No seasonality handling

- Overfitting risk with high degrees

Tips:

- Use degree = 1 (linear) unless there’s clear curvature

- Validate extrapolations carefully

- Consider ARMA for long-term forecasts

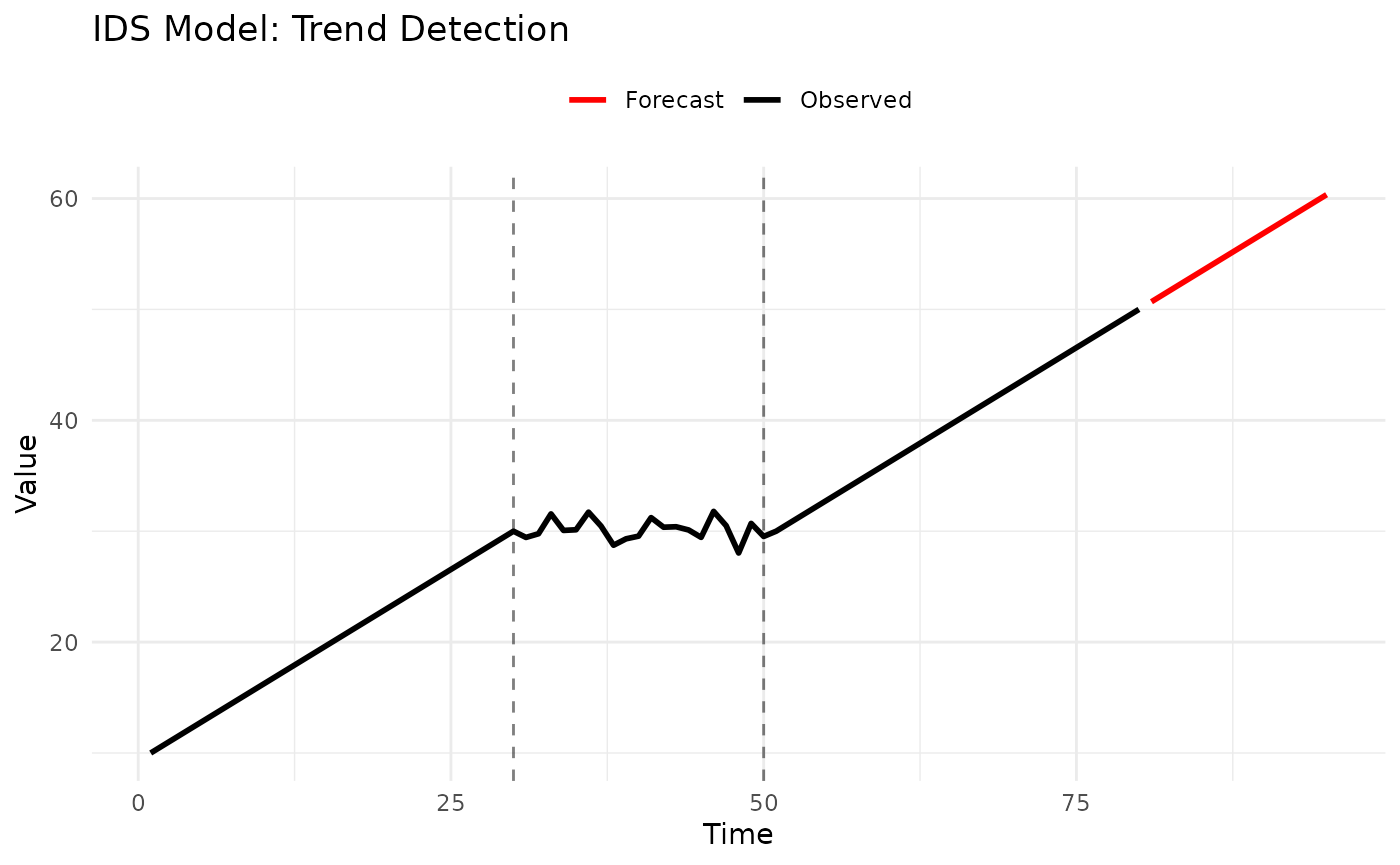

2.3 IDS Model (Increase-Decrease-Stable)

Description: Detects trend direction (increasing, decreasing, stable) over recent windows and extrapolates.

How It Works:

- Divide recent history into

pwindows - Classify each window’s trend

- Forecast based on detected pattern

When to Use:

- ✅ Step changes in trend

- ✅ Regime-switching behavior

- ✅ Need trend detection

- ❌ Smooth continuous trends (use OLS)

- ❌ Seasonal patterns

Parameters:

-

window_size: Number of windows to analyze (default: 3) -

threshold: Threshold for detecting changes (default: 0.0)

Example:

# Generate data with trend change

set.seed(123)

data <- c(

seq(10, 30, length.out = 30), # Increasing

rep(30, 20) + rnorm(20, sd = 1), # Stable

seq(30, 50, length.out = 30) # Increasing again

)

# Fit IDS model

model <- IDSModel(window_size = 3) # Analyze last 3 windows

fitted <- fit_baseline(data, model)

# Forecast

fc <- forecast(fitted, interval_method = NoInterval(), horizon = 1:15)

# Plot

n_data <- length(data)

plot_df <- rbind(

data.frame(time = 1:n_data, value = data, type = "Observed"),

data.frame(time = 81:95, value = fc$mean, type = "Forecast")

)

ggplot(plot_df, aes(x = time, y = value, color = type)) +

geom_line(linewidth = 1) +

geom_vline(xintercept = c(30, 50), linetype = "dashed", alpha = 0.5) +

scale_color_manual(values = c("Observed" = "black", "Forecast" = "red")) +

labs(title = "IDS Model: Trend Detection", x = "Time", y = "Value", color = NULL) +

theme_minimal() +

theme(legend.position = "top")

Parameter Guidance:

-

p(number of windows):- 2-3: More reactive to recent changes

- 4-6: More stable, less reactive

- Too large: Misses recent trends

Strengths:

- Detects trend changes

- Adapts to regimes

- Interpretable classifications

Limitations:

- Discrete trend categories

- Needs sufficient data

- No seasonality

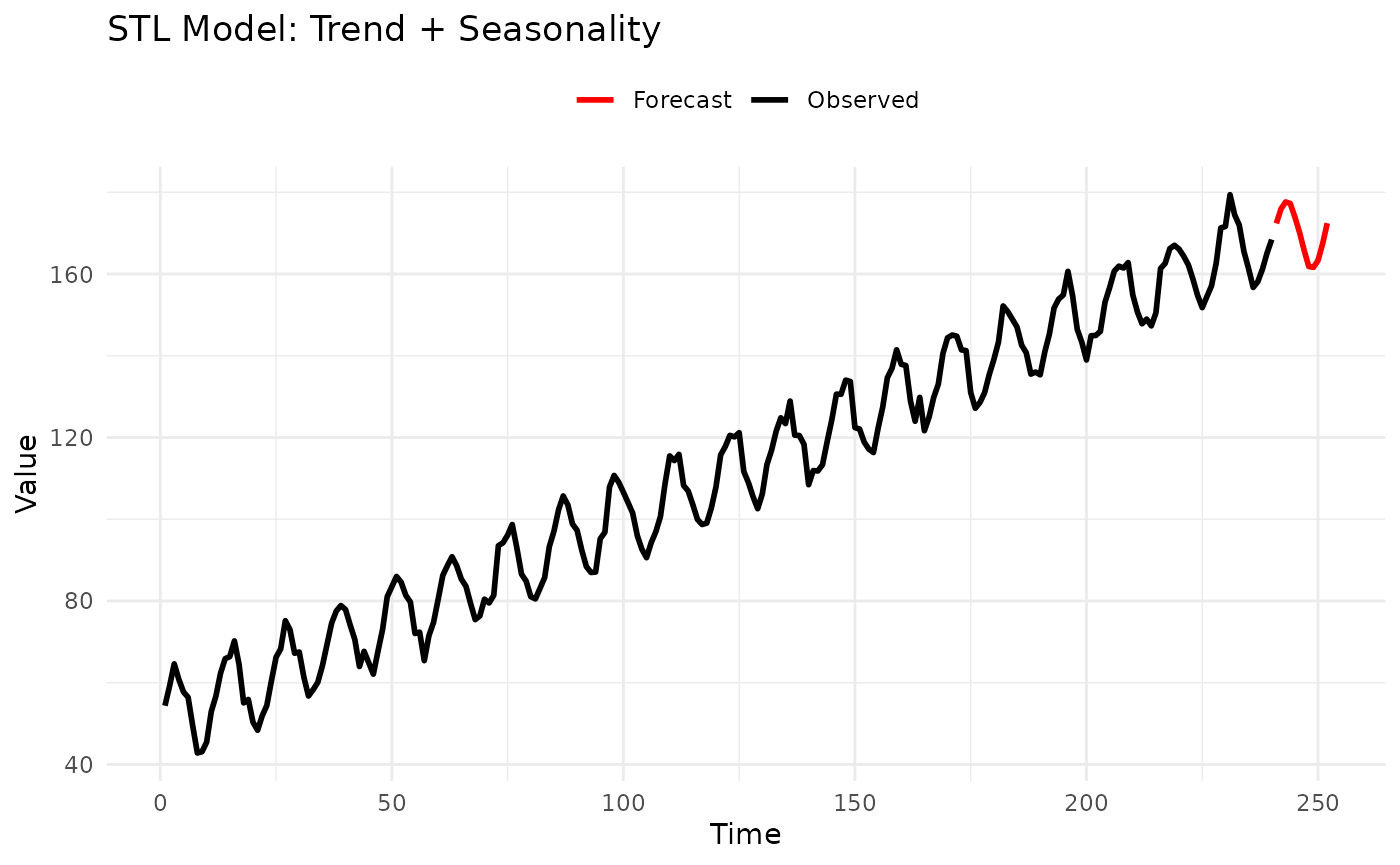

2.4 STL Model (Seasonal-Trend Decomposition)

Description: Decomposes series into seasonal, trend, and remainder components using LOESS, then forecasts each separately.

Mathematical Form:

where is trend, is seasonal, is remainder.

When to Use:

- ✅ Both trend AND seasonality

- ✅ Need decomposition for interpretation

- ✅ Regular seasonal patterns

- ❌ Irregular seasonality

- ❌ Less than 2 seasonal cycles

Parameters:

-

s: Seasonal period

Example:

# Generate trend + seasonality

set.seed(123)

time <- 1:240 # 20 years of monthly data

trend <- 0.5 * time

seasonal <- 10 * sin(2 * pi * time / 12)

data <- 50 + trend + seasonal + rnorm(240, sd = 2)

# Fit STL model

model <- STLModel(s = 12)

fitted <- fit_baseline(data, model)

# Forecast next year

fc <- forecast(fitted, interval_method = NoInterval(), horizon = 1:12)

# Plot

n_data <- length(data)

plot_df <- rbind(

data.frame(time = 1:n_data, value = data, type = "Observed"),

data.frame(time = 241:252, value = fc$mean, type = "Forecast")

)

ggplot(plot_df, aes(x = time, y = value, color = type)) +

geom_line(linewidth = 1) +

scale_color_manual(values = c("Observed" = "black", "Forecast" = "red")) +

labs(title = "STL Model: Trend + Seasonality", x = "Time", y = "Value", color = NULL) +

theme_minimal() +

theme(legend.position = "top")

Parameter Guidance:

-

s(seasonal period): Same as LSD model guidance

Strengths:

- Handles trend + seasonality together

- Robust to outliers

- Provides interpretable decomposition

- Can extract components for analysis

Limitations:

- Fixed seasonal period

- Needs at least 2 cycles

- More complex than LSD

Use Case: Preferred over LSD when trend is important, or when you need to analyze seasonal and trend components separately.

3. Advanced Time Series Models

Statistical models with parametric probability distributions.

3.1 ARMA Model (Autoregressive Moving Average)

Description: Classic time series model combining autoregressive (AR) and moving average (MA) components.

Mathematical Form:

where .

When to Use:

- ✅ Stationary time series

- ✅ Need parametric uncertainty

- ✅ Autocorrelation structure

- ❌ Strong trends (use differencing or detrend first)

- ❌ Seasonal patterns (use SARIMA or seasonal models)

Parameters:

-

p: Autoregressive order -

q: Moving average order

Example:

# Generate AR(1) process

set.seed(123)

n <- 200

data <- numeric(n)

data[1] <- rnorm(1)

for (i in 2:n) {

data[i] <- 0.7 * data[i - 1] + rnorm(1)

}

# Fit ARMA(2,1)

model <- ARMAModel(p = 2, q = 1)

fitted <- fit_baseline(data, model)

# Forecast with prediction intervals

fc <- forecast(

fitted,

interval_method = EmpiricalInterval(n_trajectories = 1000),

horizon = 1:20,

levels = c(0.5, 0.95),

model_name = "ARMA(2,1)"

)

# Add simulated truth and visualize with intervals

set.seed(456)

truth <- numeric(20)

truth[1] <- 0.7 * data[200] + rnorm(1)

for (i in 2:20) {

truth[i] <- 0.7 * truth[i - 1] + rnorm(1)

}

fc_truth <- add_truth(fc, truth)

fc_quantile <- scoringutils::as_forecast_quantile(fc_truth)

# Show quantile forecast structure

print(head(fc_quantile, 15))

#> observed predicted quantile_level horizon model

#> <num> <num> <num> <int> <char>

#> 1: -2.64651490 -3.06346875 0.025 1 ARMA(2,1)

#> 2: -2.64651490 -1.77042789 0.250 1 ARMA(2,1)

#> 3: -2.64651490 -1.21971720 0.500 1 ARMA(2,1)

#> 4: -2.64651490 -0.55847786 0.750 1 ARMA(2,1)

#> 5: -2.64651490 0.92350244 0.975 1 ARMA(2,1)

#> 6: -1.23078488 -2.54894033 0.025 2 ARMA(2,1)

#> 7: -1.23078488 -1.33700718 0.250 2 ARMA(2,1)

#> 8: -1.23078488 -0.74279283 0.500 2 ARMA(2,1)

#> 9: -1.23078488 -0.01561537 0.750 2 ARMA(2,1)

#> 10: -1.23078488 1.70207148 0.975 2 ARMA(2,1)

#> 11: -0.06067475 -2.34241843 0.025 3 ARMA(2,1)

#> 12: -0.06067475 -1.11061984 0.250 3 ARMA(2,1)

#> 13: -0.06067475 -0.54841015 0.500 3 ARMA(2,1)

#> 14: -0.06067475 0.19197878 0.750 3 ARMA(2,1)

#> 15: -0.06067475 2.24735108 0.975 3 ARMA(2,1)Parameter Guidance:

How to choose p and q:

- Plot ACF/PACF (in R):

- ACF/PACF patterns:

- ACF cuts off at lag q → MA(q)

- PACF cuts off at lag p → AR(p)

- Both decay slowly → ARMA(p,q)

- Common starting points:

- ARMA(1,0) = AR(1): Simple persistence

- ARMA(0,1) = MA(1): Single shock memory

- ARMA(1,1): Most parsimonious mixed model

- ARMA(2,2): More flexibility

- General guidance:

- Start small (p=1, q=1)

- Rarely need p or q > 3

- More parameters ≠ better forecasts

Strengths:

- Well-established theory

- Parametric uncertainty

- Efficient for stationary data

- Many diagnostic tools

Limitations:

- Requires stationarity

- Parameter selection can be tricky

- Needs sufficient data (50+)

Tips:

- Detrend before fitting if trending

- Use AIC/BIC for model selection

- Check residuals for white noise

3.2 INARCH Model (Integer ARCH)

Description: Designed for count data (non-negative integers), models conditional mean and variance with ARCH-type dynamics.

Mathematical Form:

When to Use:

- ✅ Count data (0, 1, 2, 3, …)

- ✅ Non-negative integers

- ✅ Overdispersion

- ✅ Time-varying variance

- ❌ Continuous data

- ❌ Negative values

Parameters:

-

p: Order of lags -

s: Seasonal period (optional)

Example:

# Generate count data

set.seed(123)

# Simulate Poisson AR process

lambda <- 10

data <- numeric(100)

data[1] <- rpois(1, lambda)

for (i in 2:100) {

mu <- 5 + 0.5 * data[i - 1]

data[i] <- rpois(1, mu)

}

# Fit INARCH(1)

model <- INARCHModel(p = 1)

fitted <- fit_baseline(data, model)

# Forecast

fc <- forecast(fitted, interval_method = NoInterval(), horizon = 1:10)

# Forecasts are counts

print(fc$mean)

#> [1] 8.771931 9.145271 9.325835 9.413164 9.455401 9.475828 9.485708 9.490486

#> [9] 9.492797 9.493915Parameter Guidance:

-

p(lag order):- 1: Most common, captures direct persistence

- 2-3: If ACF shows higher-order dependence

- Rarely need p > 3

-

s(seasonality):- Omit if no seasonality

- Set to period if seasonal counts

Strengths:

- Designed for count data

- Respects non-negativity

- Handles overdispersion

- Seasonal version available

Limitations:

- Only for integer counts

- Requires more data than ARMA

- Limited to Poisson/NegBin distributions

Use Cases:

- Disease counts

- Customer arrivals

- Event occurrences

- Web traffic hits

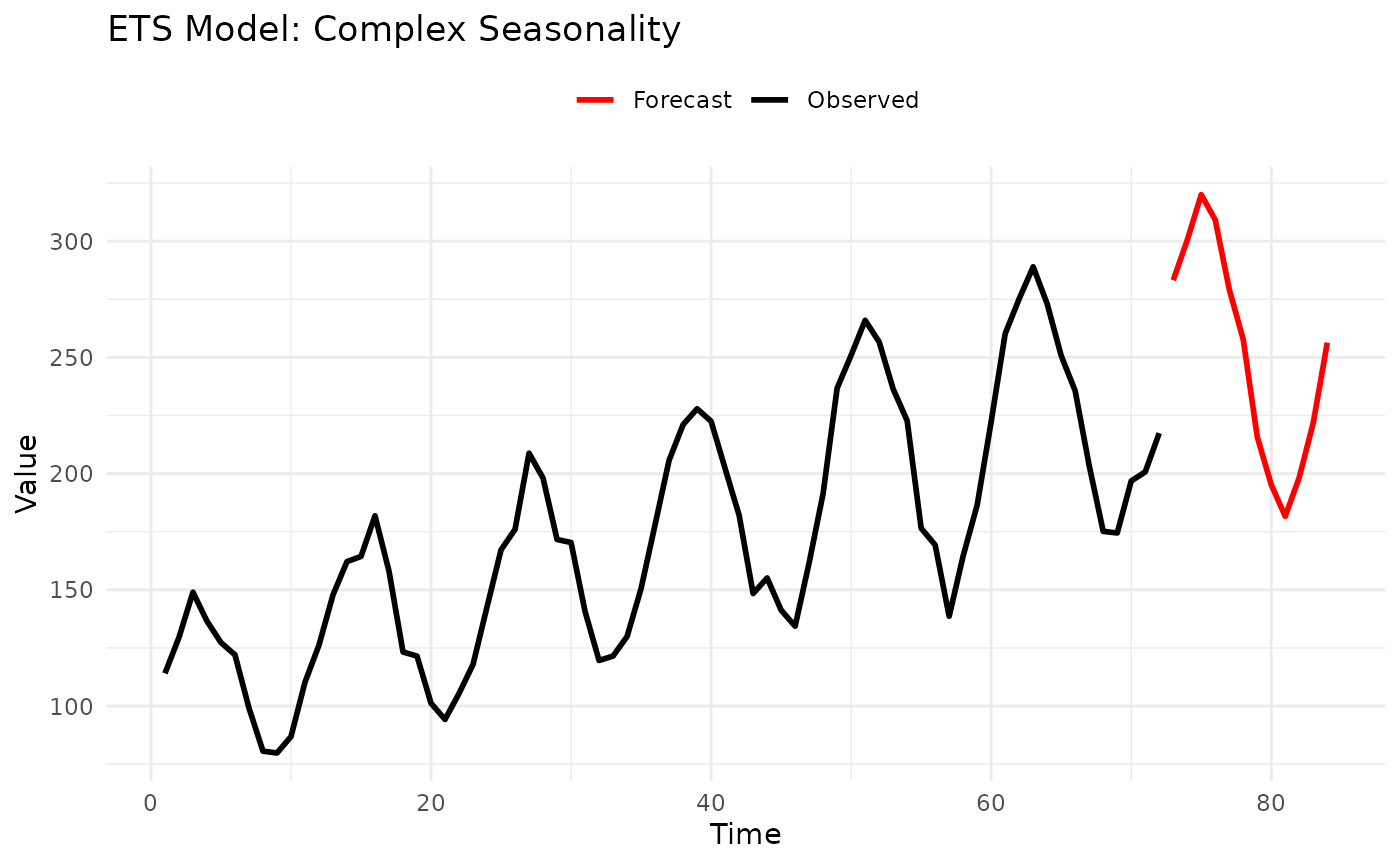

3.3 ETS Model (Error-Trend-Season)

Description: Exponential smoothing state space models covering 30 different combinations of error, trend, and seasonal components.

Components:

- Error: Additive (A) or Multiplicative (M)

- Trend: None (N), Additive (A), Multiplicative (M), Damped (Ad, Md)

- Season: None (N), Additive (A), Multiplicative (M)

When to Use:

- ✅ Complex seasonal patterns

- ✅ Need automatic model selection

- ✅ Business forecasting

- ✅ Various data characteristics

- ❌ Very short series (< 2 cycles)

- ❌ Need interpretable parameters

Parameters:

-

error: “A” (additive) or “M” (multiplicative) or NULL (auto) -

trend: “N”, “A”, “M”, “Ad”, “Md”, or NULL (auto) -

season: “N”, “A”, “M”, or NULL (auto) -

s: Seasonal period (if seasonal)

Example:

# Generate multiplicative seasonal data

set.seed(123)

time <- 1:72

trend <- 100 + 2 * time

seasonal_mult <- 1 + 0.3 * sin(2 * pi * time / 12)

data <- trend * seasonal_mult * exp(rnorm(72, sd = 0.05))

# Automatic selection

model_auto <- ETSModel()

fitted_auto <- fit_baseline(data, model_auto)

# Specific: Multiplicative error, additive trend, multiplicative season

model_specific <- ETSModel(error_type = "M", trend_type = "A", season_type = "M", s = 12)

fitted_specific <- fit_baseline(data, model_specific)

# Forecast

fc <- forecast(fitted_specific,

interval_method = NoInterval(),

horizon = 1:12

)

# Plot

n_data <- length(data)

plot_df <- rbind(

data.frame(time = 1:n_data, value = data, type = "Observed"),

data.frame(time = 73:84, value = fc$mean, type = "Forecast")

)

ggplot(plot_df, aes(x = time, y = value, color = type)) +

geom_line(linewidth = 1) +

scale_color_manual(values = c("Observed" = "black", "Forecast" = "red")) +

labs(title = "ETS Model: Complex Seasonality", x = "Time", y = "Value", color = NULL) +

theme_minimal() +

theme(legend.position = "top")

Model Selection Guide:

Error type:

- Additive (A): Errors independent of level

- Multiplicative (M): Errors proportional to level

Trend type:

- None (N): No trend

- Additive (A): Linear trend

- Multiplicative (M): Exponential trend

- Additive Damped (Ad): Trend decays to flat

- Multiplicative Damped (Md): Trend decays exponentially

Season type:

- None (N): No seasonality

- Additive (A): Constant seasonal fluctuation

- Multiplicative (M): Seasonal % of level

Common Models:

-

ETS(A,N,N): Simple exponential smoothing -

ETS(A,A,N): Holt’s linear trend -

ETS(A,A,A): Additive Holt-Winters -

ETS(A,A,M): Multiplicative seasonality -

ETS(M,M,M): Fully multiplicative

Strengths:

- Extremely flexible (30 models)

- Automatic selection available

- Well-tested in practice

- Handles many data types

Limitations:

- Many parameters to choose

- Computationally intensive

- Less interpretable than ARMA

- Can overfit

Tips:

- Start with automatic selection (NULL parameters)

- Use additive for stable variance

- Use multiplicative for percentage seasonality

- Damped trends for long horizons

Model Selection Examples

Example 1: Monthly Sales Data

# Simulated retail sales: trend + seasonality + promotions

set.seed(123)

months <- 1:240

trend <- 1000 + 20 * months

seasonal <- 200 * sin(2 * pi * months / 12) # Holiday peaks

noise <- rnorm(240, sd = 50)

data <- trend + seasonal + noise

# Try multiple models

models <- list(

Naive = ConstantModel(),

LSD = LSDModel(window_width = 3, s = 12),

STL = STLModel(s = 12),

ETS = ETSModel(error_type = "A", trend_type = "A", season_type = "A", s = 12)

)

# Fit all models

results <- lapply(names(models), function(name) {

fitted <- fit_baseline(data, models[[name]])

fc <- forecast(fitted, interval_method = NoInterval(), horizon = 1:12)

data.frame(

Model = name,

Forecast_Mean = mean(fc$mean)

)

})

comparison <- do.call(rbind, results)

print(comparison)

#> Model Forecast_Mean

#> 1 Naive 5760.923

#> 2 LSD 3417.800

#> 3 STL 5858.771

#> 4 ETS 5924.238

# Recommendation: STL or ETS for trend + seasonalityExample 2: Website Traffic (Count Data)

# Daily page views (count data)

set.seed(456)

days <- 100

data <- rpois(days, lambda = 100 + 0.5 * 1:days)

# Count-specific models

models <- list(

Marginal = MarginalModel(), # Ignore trend

INARCH = INARCHModel(p = 1) # Model count dynamics

)

# Compare

# INARCH should perform better due to trend

# Recommendation: INARCH for count data with patternsExample 3: Financial Returns

# Daily returns (stationary, no trend/season)

set.seed(789)

data <- rnorm(200, mean = 0.001, sd = 0.02)

# Stationary models

models <- list(

Marginal = MarginalModel(),

ARMA = ARMAModel(p = 1, q = 1)

)

# For returns, ARMA captures autocorrelation

# Marginal is baseline

# Recommendation: ARMA if autocorrelation present, else MarginalPerformance Considerations

Summary and Recommendations

Quick Start

Don’t know where to begin?

- Start with

ConstantModel()- it’s fast and shows what “no model” looks like - If you have seasonality, try

STLModel(s = period) - If stationary without seasonality, try

ARMAModel(p = 1, q = 1) - Compare models with

score()functions

Best Practices

- Always use a simple baseline - ConstantModel or Marginal

- Match model to data characteristics:

- Counts → INARCH

- Seasonal → STL or LSD

- Stationary → ARMA

- Complex → ETS

- Validate on holdout data - use

truthparameter - Check residuals - should look like white noise

- Start simple, add complexity only if needed

Further Reading

- See

vignette("forecastbaselines")for basic workflow - See

vignette("transformations")for data preprocessing - Check individual function help:

?ARMAModel,?forecast, etc.

Appendix: Parameter Quick Reference

# Simple Baselines

ConstantModel()

MarginalModel()

KDEModel()

# Seasonal/Trend

LSDModel(window_width = 3, s = 12)

OLSModel(degree = 1, differencing = 0)

IDSModel(window_size = 3)

STLModel(s = 12)

# Advanced

ARMAModel(p = 1, q = 1)

INARCHModel(p = 1, s = NULL)

ETSModel(error_type = "A", trend_type = "N", season_type = "N", s = NULL)